17 Oct Allocation Difference in ASC 606 / IFRS 15 Vs Ind AS 18

Revenue is an important point of concern to the users of Financial Statements in assessing an entity’s Financial Performance and Position.

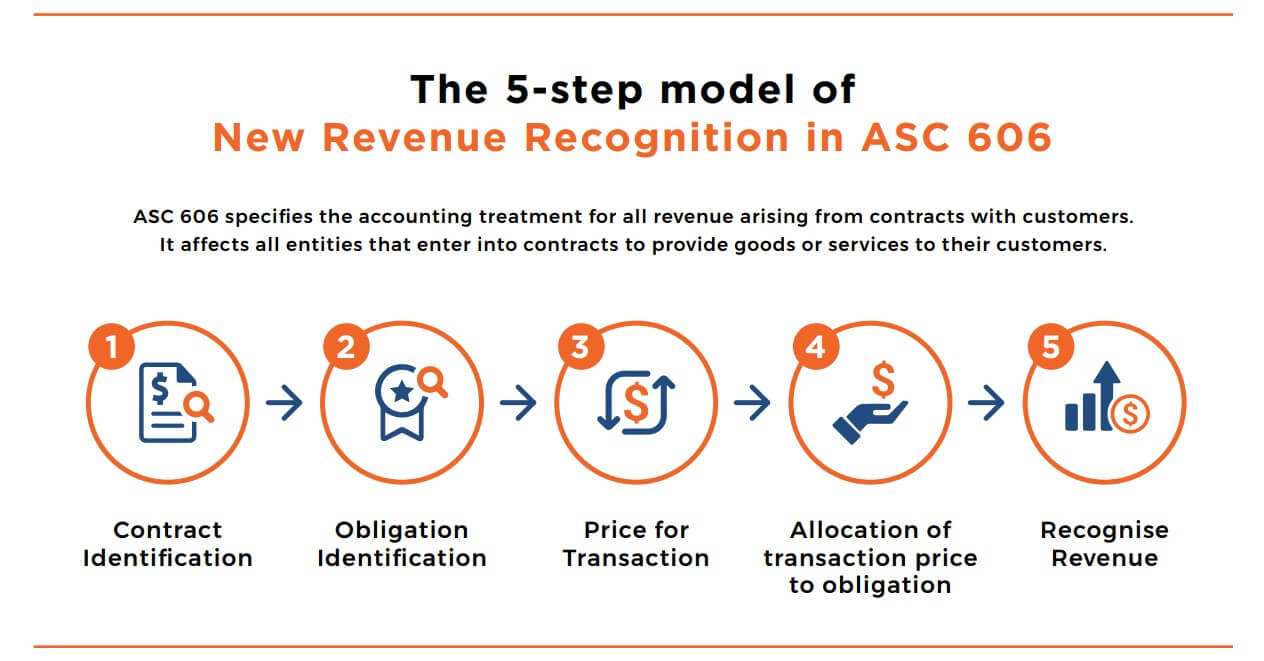

Accounting Standard Codification (ASC) 606 – Revenue from Contract with Customers is an Industry-wide revenue recognition guidance which has been formulate by Financial Accounting Standard Board (FASB). This was a joint task by Financial Accounting Standard Board (FASB) and International Accounting Standard Board (IASB) to clarify the principles for Revenue Recognition and to develop common revenue standard for U.S. GAAP and IFRS.

ASC 606 will be applicable across all the industries and aid in recognizing revenue from all the types of transactions, except those transactions which are covered by more specific guidelines (for example – Insurance Contract or Leasing Contract).

Ind AS 18

Like ASC 606 and IFRS 15, India too has accounting standards that provide guidelines for standardized revenue recognition to simplify taxation in India’s burgeoning economy, and this standard is known as the Ind AS 18. Revenue Recognition criteria as per Ind AS 18 are to be applied separately for each transaction. However, components of the transactions which are required to be assessed separately can be assessed as a bundle provided they are identifiable as components of single transaction. This is required to be recognized to depict the substance over form of that transaction.

For example, If a product is sold with subsequent ‘after-sales services’ revolving around the good, then as per Ind AS 18, ‘Arm’s Length Price’ or FV of such services should be considered and revenue should be deferred over the period during which the service is performed or meant to be performed.

Unfortunately, this standard lacked convergence with global accounting standard such like IFRS15 which talks about the “5 step model” approach towards revenue recognition. To come to par with International RevRec standards, The Ministry of Corporate Affairs (MCA), on 28th Mar,2018, has notified that Ind AS 115 (Revenue from contract with customers) is in effect from 1st April 2018 and will replace the old standards Ind AS 11 (Construction Contracts) and Ind AS 18 (Revenue).

ASC 606/IFRS 15

In ASC 606 and IFRS 15, Revenue recognition criteria are applied separately for each Performance Obligation (POB). Each transaction is bifurcated into separate POB and in some cases multiple transactions are also clubbed into a single POB depending on the nature of the service or the nature of contract. ASC 606/IFRS 15 identifies Standalone selling price (SSP) for each transaction and allocates the transaction price in the ratio of SSP. Once allocation of amount is made to the transactions, revenue is recognized for the allocated amount as and when the corresponding performance obligation is satisfied.

Identification of POB and determination of transaction price in ASC 606/IFRS 15 makes it an excellent standard but ascertaining standalone selling price can be subjective due to unavailability of data or uniqueness of products or services. The Standard provides no guidance when SSP is not observable but requires accountants to make an estimate considering the below factors:

- Market price adjusted for similar goods and services

- Cost + Margin

- Residual approach (Expected to apply in very rare situation)

Considering the above points, there are a myriad of other factors that affect estimation of SSP for products and make it tougher to be accurate are price differences in different geographies, Inflation in different geographies, Market penetration policies etc.….

Product life-cycle also makes it difficult for deriving the SSP/ to make allocation of revenue for recognition in the first place. In today’s dynamic economic environment, even though SSP is derived from historical transaction, it needs regular amendments as prices constantly fluctuate based on time and region. These changes should also be incorporated by the entities to give accurate reporting of Revenue and its allocation.

Due to above challenges, IFRS 15 has been globally welcomed by the Accounting Industry as it eases the norms of doing business. Better Internal Controls would reduce the risk of Financial Reporting and help operators to be aligned with Sarbanes Oxley Require-ments. ASC 606 and IND AS 115, on the other hand, are promulgated considering their local reporting requirements/situations exist-ing in their respective countries.

#RevenueRecognition #RevRec #IFRS15 #ASC606 #IndAS115

Did you find this article helpful?

We will be happy to answer any questions/queries regarding this and any other topics regarding Revenue Recognition and ASC 606.